National Pension Scheme (NPS) is a voluntary retirement scheme which aimed to secure future in the form of Pension. The main aim of this scheme is to provide regular income after the retirement to the contributors. Governing body of this scheme is PFRDA (Pension Fund Regulatory and Development Authority). This is a long term investment plan and initiated by the central Government.

There are two types of account under NPS

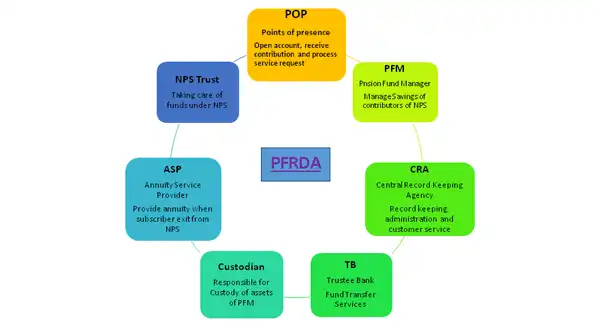

NPS Administration Structure

A Citizen of India age between 18-70 years can open NPS account. This pension program is open to employees from the public, private and for unorganized sector also.

Active Choice: In this option subscriber have the option to decide where he want to invest his fund.

There are various funds available under active choice option of National Pension Fund (NPS)

Auto Choice (Lifecycle Fund): NPS offers an easy option for those participants who do not have the required knowledge to manage their NPS investments.In this option, the investments will be made in a life-cycle fund.

In auto choice option 3 life cycle funds are available.

If subscriber not choose any option mentioned above than default auto choice will be provided which is moderate option.

3. Liquidity: Under liquidity option both partial withdrawal and Exit is allowed in National Saving plan (NPS).

(b) Exit from Scheme: There are 3 types to exit.

Upon reaching 60 years:

Exit before reaching 60 Years (Voluntary Retirement)

Upon death:

However, the subscriber has the option to defer the lump sum withdrawal till the age of 75 years. This option is required to be exercised up to 15 days prior to completion of 60 years.

4. Flexibility: NPS scheme is very flexible. It is providing many options and features.

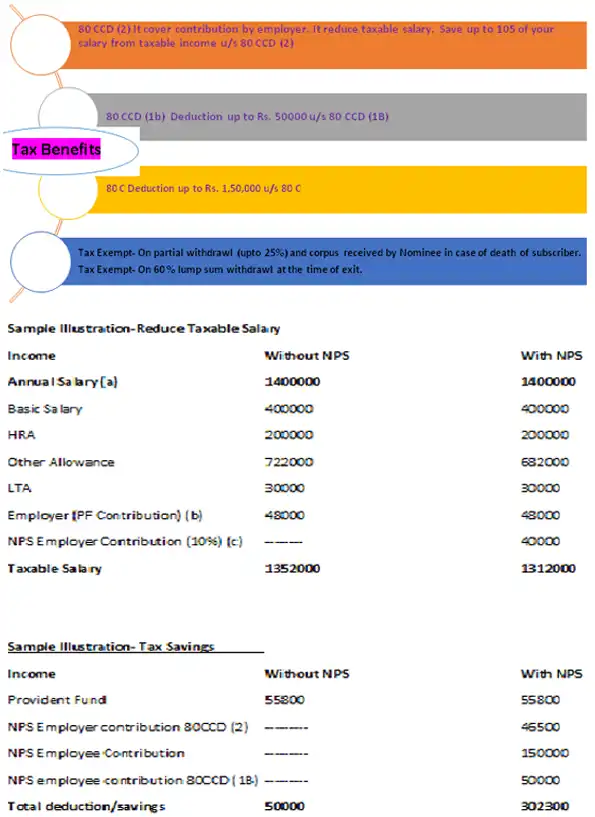

Tier I: Thisaccount is called pension account. In this contribution of Rs. 50000 is eligible for tax deduction under section 80CCD (1B). This is extra and above the limit of Rs. 1.50 Lacs under section 80C.

Tier II: Additional amount can be investing in this account. In this subscriber is completely free to withdraw any amount at any point of time. This amount is not eligible for tax benefits. Tier II amount can be transfer to Tier I.

| Particulars | Tier I (Rs.) | Tier II (Rs.) |

|---|---|---|

| Minimum amount to open account | 500 | 1000 |

| Minimum amount to contribute every year | 1000 | N.A |

| Minimum subsequent contribution | 500 | 250 |

5. Portable:

It is portable scheme; you can operate your NPS account anywhere in the country. Contribution can be made from any POP-SP branch. NPS account can be transfer from one sector to another sector like government Sector to private sector or from one employer to another employer in same sector.

6. Low Costing:

NPS is considered to be the world’s lowest cost pension scheme. Administrative charges and fund management fee are also lowest.

7. Some other Features:

National Pension System (NPS) is based on unique Permanent Retirement Account Number (PRAN) which is allotted to every subscriber. In order to encourage savings, the Government of India has made the scheme reassuring from security point of view and has offered some attractive benefits for NPS account holders.

This is a unique number provided to subscriber of NPS account. You can get your PRAN by following below mentioned steps.